Time Value of Money Calculator

Online TVM solver to easily calculate the future value, present value, interest rate, or the required repeating payment. TVM calculator applicable to deposits, credits, investments, retirement portfolios, and others.

- How to use the TVM calculator

- TVM Formula

- Understanding the Time Value of Money

- Example use in retirement planning

- Financial caution

How to use the TVM calculator

Our online calculator makes it simple and easy to calculate various quantities related to the time value of money such as present value, future value, interest rate, and periodical cash flows.

The repeating payments field (labeled "Cash flows") is optional. These can be payments to periodically cover a loan, or deposits to increase a deposit's value each month or each year. These could also be contributions to a 401k or paying into another type of investment. If left empty or set to zero, it means there are no expected top ups or withdrawals during the entire time period.

The input in the interest rate field in the calculator needs to be the effective interest rate based on the period for which you are performing the calculation. If the period is a year (e.g. you've entered "5" for the "Number of periods" field and this is a 5-year loan) then you should enter the effective annualized interest rate. If the period is a month, you should enter the effective monthly interest rate instead.

The TVM formula calculator can solve for:

- present value

- future value

- number of periods

- required rate of interest

- the value of each payment in a compounding period

After deciding what you want to solve for in the TVM equation, provide the remaining values and press "Calculate". Consult the question marks next to each field's label if you are uncertain on how to proceed.

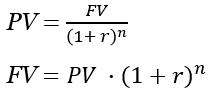

TVM Formula

The calculation of time value of money depends on the following inputs: present value (PV), future value (FV), the value of the individual payments in each compounding period (A), the number of periods (n), the interest rate (r).

You can use the following two formulas to calculate present value and future value without periodical payments [1][2]:

If there are periodical payments (cash inflows or outflows) they need to be adjusted similar to the present value / future value and added to the formulas above. Calculating the amount of the periodical payment required is a simple analytical transformation handled by the TVM solver automatically.

Calculating the number of periods or the interest rate however is not trivial as there is no analytical solution. It must therefore be done through successive approximation until a reasonably accurate value is pinpointed. Our time value of money calculator can easily do this for you.

More complex formulas can include growing instead of fixed periodical payment (g), but this is not supported in our tool at the present.

Understanding the Time Value of Money

The concept of how the value of money depends on the timeline reflects the fact that humans have what in finance is called "time preference". In the simplest terms, given identical gains, people would rather take them now rather than later. For example, if you can get $10,000 now or in 5 years, you'd choose to get them now, all other things being equal. This stems both from the ability to spend the money immediately (almost certain benefit) versus the uncertainty related to spending them in 5 years, eventually. Similarly, if you invest the money or put it in a bank deposit they can earn you interest during these 5 years: something you would not be able to do otherwise. Time-related opportunity costs are the reason the concept of time value of money is key in managing personal or business finances.

Time preference is the reason for interest rates to exist: they are in fact the "price" paid for using money in a given period of time. It compensates the depositor or lender for their opportunity cost. Consequently, interest rates are low when the perceived opportunity cost is low and high if they are high. Similarly, investors inform their decisions on whether to pass or get in a certain venture by calculating the expected return (increase in value of their capital) versus alternative investments.

Example use in retirement planning

The role of the time value of money when planning a retirement is in understanding the future value of a given sum invested in present time. The central idea is that $1,000 today has a future value of significantly more than $1,000 due to compounding, even when adjusted for inflation. A TVM calculator can help you understand how your retirement capital will grow in value if it accumulates compounding returns such as those obtained from investments in stocks, mutual funds, systemic investment plans (SIP), or the compounding interest on a certificate of deposit.

Future value with compounding returns

For example, consider setting aside $10,000 that earn the average S&P 500 return of 8% until your retirement. If you begin 10 years before your retirement, that $10,000 will grow to $21,589, or just over two times more. However, if you begin 30 years before retirement that same $10,000 would be $100,626 or nearly ten times more than the initial investment. Add $1,000 a year to the initial fund and by year 30 you would be looking at $213,909 in your retirement portfolio.

Withdrawal planning

Another way to use time value of money is to calculate how much money you would have left say 20 years into your retirement, assuming monthly withdrawals. If you begin with $250,000 of retirement savings and withdraw a periodic payment of $2,000 each month or $24,000 annually. How much money would you have left after 20 years? Use our TVM calculator to calculate the future value of the fund, which in this case amounts to $66,952 (see calculation).

Financial caution

This is a simple online tool which is a good starting point in estimating different quantities related to financial planning such as making an investment or taking a credit, but is by no means the end of such a process. You should always consult a qualified professional when making important financial decisions and long-term agreements, such as long-term bank deposits. Use the information provided by the solver critically and at your own risk.

References

1Desai M. A. (2019). "How Finance Works: The HBR Guide to Thinking Smart about the Numbers". Harvard Business Review Press. pp.72-75

2Damodaran, A. (2012). "Investment Valuation: Tools and Techniques for Determining the Value of Any Asset" (3rd edition). John Wiley & Sons. pp.11-13

Cite this calculator & page

Cite results from this online calculator or information on this page by choosing a citation format:

Georgiev, G.Z. (n.d.). Time Value of Money Calculator. GIGAcalculator.com. Retrieved Jun 29, 2026, from https://www.gigacalculator.com/calculators/time-value-of-money-calculator.php