Investment professionals and individual investors often need to estimate the profitability of a given investment opportunity, or to retrospectively assess the results of past investments. This is typically done with the idea of comparing two or more opportunities and deciding which one to choose. Think two or more mutual funds, hedge funds, stocks, systematic investment plans (SIPs), or business projects.

All other things being equal, the annual growth of an investment is a leading measure by which such comparisons are made. However, calculating said return is not always as trivial and therefore there exist different ways to do it. Different types of returns are applicable to different investments, as well as whether or not the time value of money is taken into account.

Simple financial measures include:

- absolute return

- relative return

- periodic returns

More complex metrics include:

- CAGR (Compound Annual Growth Rate)

- IRR (Internal Rate of Return)

- XIRR (Extended Internal Rate of Return)

Each measure has its use case, depending mostly on the time to return, as well as the number and timings of cash flow events. Another key aspect is whether the investment returns are compounding or not.

CAGR vs IRR vs XIRR Cheat Sheet

The table below shows key differences between CAGR, IRR, and XIRR, and when to use each:

| Measure / Characteristics of Investments to Compare | Time to return | Cash flow events | Type of return |

|---|---|---|---|

| Absolute return | Same | One outflow, one inflow each | Compounding or Non-compounding |

| Relative return (%) | Same | One outflow, one inflow each | Compounding or Non-compounding |

| Simple Annualized Return | Different | One outflow, one inflow each | Non-compounding |

| CAGR | Different | One outflow, one inflow each | Compounding |

| IRR | Different | Multiple outflows and/or inflows at regular intervals | Compounding |

| XIRR | Different | Multiple outflows and/or inflows at regular or irregular intervals | Compounding |

Absolute and relative return are useful to an investor if the time to return of multiple investments of interest is exactly the same, and there is just one outflow (the initial investment) and one inflow at the end. The return can be either compounding or non-compounding within the investment term.

When the time to return is different across investment opportunities, annualized measurements are appropriate. Both CAGR and Simple annualized return work when there are only two cash flow events. The former is suitable for compounding returns and the latter for non-compounding ones.

When there are multiple cash flow events IRR becomes necessary. XIRR is an extension of IRR computed in a way which allows for non-periodic cash flows.

While this is a brief comparison of CAGR, IRR, XIRR, and simpler measures of profitability such as absolute return and a simple annualized return, you may find it beneficial to dig deeper into the calculation methods and assumptions behind each. Before we start discussing these advanced topics in more detail, it is useful to consider why we need them in the first place.

What Type of Return to Calculate?

For really short-term investments, one can simply compute the absolute return. For example, if you invest $10,000 in a mutual fund and get $15,000 in a couple of days, you might as well not bother with more complex measures. Just compute the absolute return which is just $15,000 – $10,000 = $5,000, or transform it into a percentage as such:

$5,000 / $10,000 x 100(%) = 0.5 x 100(%) = 50%

The above is just the “X is what percent of Y?” percentage calculation. So, $5,000 return on an investment of $10,000 is equal to 50% relative return. In other words, the rate of return is fifty percent.

Obviously, such investments rarely, if ever, occur in practice. Typically, a fifty percent return on the value of the investment can be expected to take several years to achieve. Different investments take different amounts of time for returns to accumulate which is why it is useful to have a measure which makes multiple investments with different time to return comparable.

Annualized Returns

Calculating the average return on a per year basis is useful to compare the value of investments with different time spans. Say there are two investments with identical absolute return of $5,000 and relative return of 50%. However, Investment A takes two years before payback day whereas Investment B takes five years before one can get said return on investment.

All other things being equal, the time preference of investors dictates that one would prefer to get their return back sooner rather than later. This is easily captured by calculating the simple annualized rate of return using the formula Relative Return / Number of Years:

- For Investment A: 50% / 2 = 25% per year ($5,000 / 2 = $2,500 per year in absolute terms)

- For Investment B: 50% / 5 = 10% per year ($5,000 / 5 = $1,000 per year in absolute terms)

Note that you might also encounter the “per annum” wording, which is Latin for “per year”, and is often abbreviated as “p.a.”. That is just the annual rate of return. Also note that returns can also be calculated on a quarterly, monthly, or even weekly basis in much the same way, though these would be less common.

The issue with simple annualized returns is that most investments do not pay in such a manner. Returns are compounded annually, year after year. This is true of stock market investments, mutual funds, certificates of deposit, and many other bank products and investment products such as a SIP. Such scenarios call for compound rates of return.

When to Use Compound Annual Growth Rate (CAGR)

CAGR, short for “Compound Annual Growth Rate”, is the average rate of growth of the value of an asset over a given period of time. It is applicable to all kinds of assets where the returns in one year get compounded into the base of calculating the return in the years following. The most simple example of this is the familiar compound interest calculation. Other examples include investments in the stock market and various derivatives.

A fundamental assumption of CAGR is that there are just two cash flow events. The initial outflow in the first year is the investment event. Then there is an inflow in the end period in which the invested sum is returned alongside a certain profit. That is the end value received by the investor.

For the same 5-year investment as discussed in the examples above, it would look like this:

Note the absence of flows during the investment term. CAGR is an average rate of growth of the value of the investment on an annual basis with zero cash flows associated with interim periods. The calculation is therefore very simple, with the CAGR formula being:

See the “CAGR formula” section in our CAGR calculator page for details about the variables used, but it is basically just raising the relative return to the power of one divided by the number of periods. While this accounts for compounding, it leaves no room for interim cash flows.

Continuing the example with our $10,000 investment which returns $15,000 in five years time. Assume this return is achieved through yearly compounding. Then, the compound annual growth rate of the value of this investment would be 8.447%, calculated simply as (15,000 / 10,000) raised to the power of (1 / 5), minus one.

This may work for simple textbook scenarios, but most real-world applications involve multiple cash flows. For example, buying a property and selling it later with a profit may look like a case for applying CAGR. However, a more accurate model should also account for:

- maintenance

- property taxes

- miscellaneous expenses

- rent income*

* if the real estate is being rented during the investment period

More complex scenarios such as investing in a company, purchasing stocks or bonds, and so on, almost always include interim flows that increase or decrease the investment’s value. These can come in the form of dividend payments, interest rate payments, partial repayments, as well as the appreciation of the investment or capital asset.

When to Use Internal Rate of Return (IRR)

When there are periodic cash flows, e.g. annual interest being accrued or charged, annual or quarterly dividends being paid out, monthly withdrawals or contributions, etc. these need to be taken into account. It includes not just the value of returns, but also their timing. CAGR cannot capture these flows and so IRR is the correct measure of returns. Use cases include SIPs, stocks that pay out dividends, and more.

Another way to understand IRR is that it is the compound annual growth rate adjusted for the cash flows, accounting for their amount, direction, and timing. Due to the time value of money, earlier cash flows need to be weighed more heavily than later cash flows. This logic is factored in a net present value calculation. Since IRR is the return rate at which the NPV of an investment equals zero, an IRR calculation values earlier flows more than ones happening on later dates.

How to calculate IRR

The NPV formula with regular cash flow intervals is:

IRR is just solving the above equation for r with NPV equal to zero. Unlike CAGR, the IRR formula is not analytical and uses iterative summation to account for the periodic cash flows. The IRR equation when applied to a single cash outflow followed by a single cash inflow can be shown to be equivalent to the CAGR formula.

So, CAGR and IRR are exactly the same when the interim cash flows all equal zero. The internal rate of return of our example $10,000 investment calculated with zero cash flows in years one through four equals 8.447% (see this IRR calculation), which is exactly the investment’s compound annual growth rate.

CAGR vs IRR example

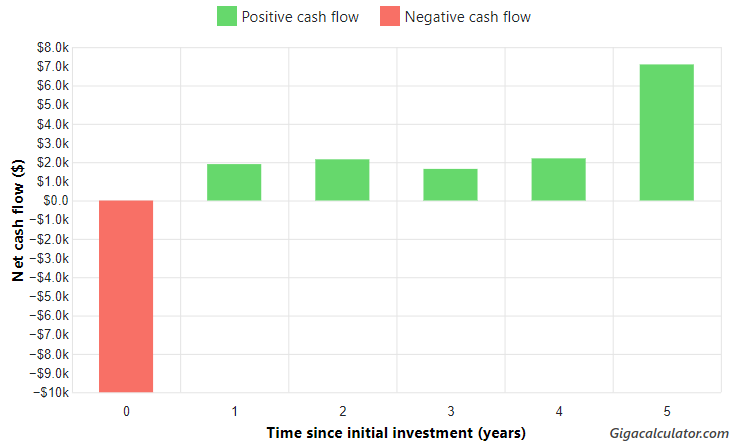

If the interim cash flows are non-zero, IRR will typically be greater than the CAGR if the earlier flows are positive, reflecting the fact that getting money out quicker is preferred by investors. In this example IRR calculation the rate of return is over 12%, despite the net cash flow (absolute return) being exactly $5,000, and the relative return being exactly 50%, just like in the original example. This is due to the significant cash inflows happening in the years before the term of the investment, namely: $1,900, $2,150, $1650, $2,200 at the end of years 1-4, and a final inflow of $7,100 at the end of year five, as plotted below:

The above example shows why it would be inappropriate to use CAGR when there are more than two cash flows and the adequate measure of returns in such cases is the IRR.

When to Use Extended Internal Rate of Return (XIRR)

XIRR can be viewed as an extension of IRR calculations for cases when the cash flows associated with an investment are irregular. Remember that an assumption of the IRR formula is that cash flow events occur at fixed time intervals. There are no such restrictions with XIRR’s since its formula accommodates irregular cash flows.

Calculating XIRR is to solve the following equation for r with NPV fixed at zero.

XIRR differs from IRR only in its allowance for non-periodic investment cash flows. Note that XIRR is an annualized rate by the above formula, but it can also be adopted for quarterly, monthly or weekly rates of return by substituting 365 with the appropriate number of days.

Viewed from a different angle, a XIRR calculation is the most generic type of compound annual growth rate calculation. IRR is a simplified version of the XIRR formula in which the timing is given as number of years (or other periods) whereas CAGR can be viewed as an IRR calculation with a single cash outflow and a single cash inflow event.

XIRR vs IRR

XIRR and IRR produce the same output if the intervals between cash flows are regular. CAGR, IRR, and XIRR will all result in the same annualized rate of return if there are only two cash flow events: an outflow followed by an inflow. This was shown in the example above where CAGR, IRR, and XIRR are all equal to 8.447% if there are no interim flows of money.

A Recap on CAGR, IRR, and XIRR

Compound annual growth rate, annualized internal rate of return and the annualized extended internal rate of return can all be viewed as simplifications of XIRR tailored to specific scenarios.

XIRR, being the most general method, is applicable for comparing compounding return investments with:

- the same of different term (holding period)

- presence or absence of cash flows of varying size

- periodic or non-periodic cash flows

In all this, XIRR calculations take into account the time preference of investors.

IRR is a simplification of XIRR in which only periodic cash flows are allowed.

CAGR is a further simplification in which just a single inflow (investment event) and a single outflow (cash out event) are allowed.

With CAGR being so simple, it barely leaves room for the time value of money, except for when it takes into account the total duration of the investment period. CAGR is therefore mostly useful when comparing things like mutual fund or investment strategy performance. IRR and especially XIRR find a greater number of practical applications due to their allowance of multiple cash flows characteristic of systemic investment plans.

That said, all of these methods suffer from a common limitation which is that they are not accounting for the riskiness of an investment or business project. They are useful in isolation (when “all else is equal”), which is a reflection of the fact that the investment performance in terms of returns represents only one part of its value. Other factors have to be taken into account when considering whether to undertake an investment or not, in comparison with other possible uses of the same capital.

If you’ve found this comparison of CAGR, IRR, and XIRR, the exploration of their differences and similarities and how they can be applied to investing useful, make sure to share it by also citing the source.

An applied statistician, data analyst, and developer of statistical software, Georgi has expertise in web analytics, statistics, design of experiments, and business risk management, among others. He covers a variety of topics where mathematical models and statistics are useful and loves to build calculators which solve apply these models in practice. Georgi is also the author of the influential book “Statistical Methods in Online A/B Testing” (2019).